Strategy

ASI’s Strategy and Theory of Change guide our focus and progress.

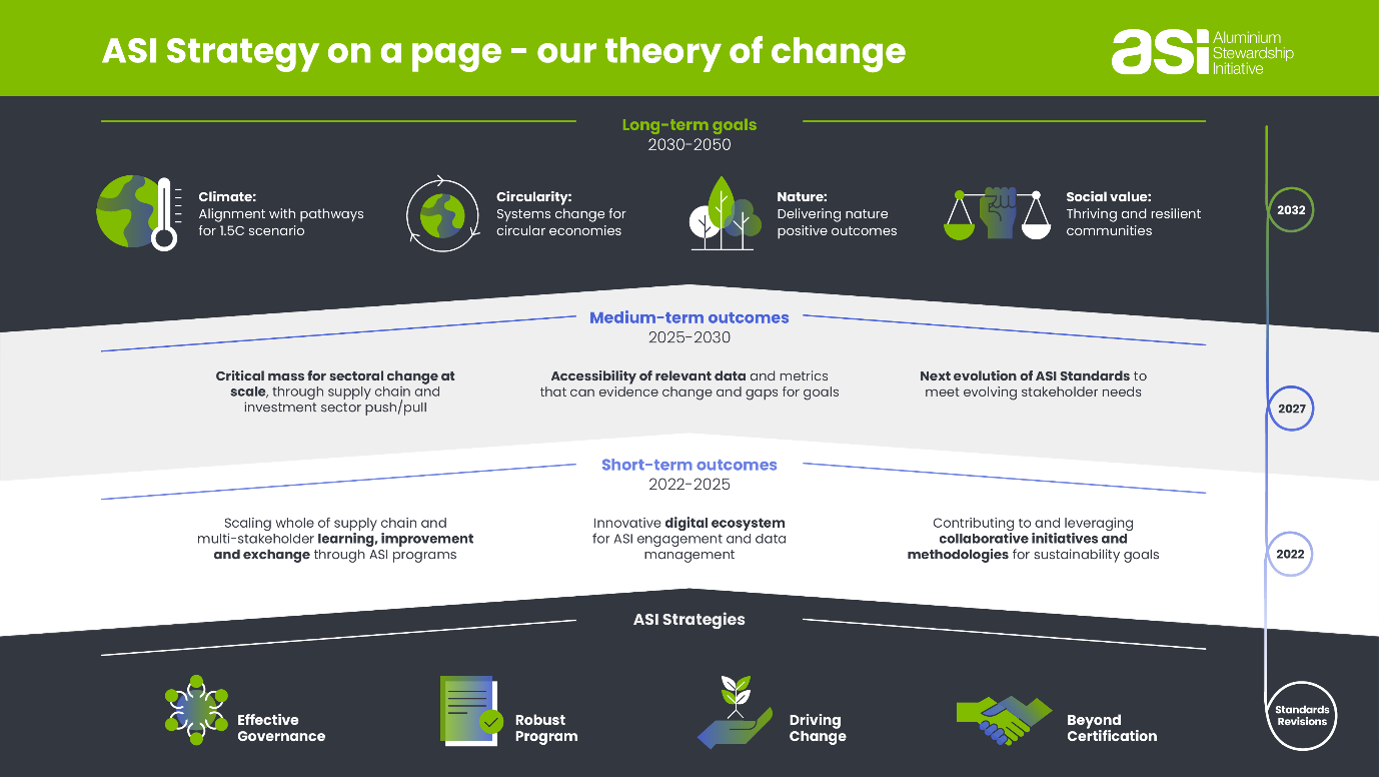

Strategy on a page

ASI’s Strategy on a page illustrates our ‘theory of change’ out to 2050 – the mechanisms through which we aim to contribute to sustainability-enhancing changes in the aluminium sector.

ASI’s four strategic foundations

Effective Governance plays an enabling foundation for ASI’s work, with a focus on multi-stakeholder decision-making at a standards and corporate governance level, as well as organisational and financial resilience.

Robust Program provides the technical foundation for delivering quality implementation of agreed standards and supporting the integrity of assurance frameworks by members and auditors.

Driving Change highlights the critical role of data and transparency to track progress, deepen insights and bring together the necessary actors to ultimately catalyse sustainability sector transformation on key sustainability topics.

Beyond Certification recognises that ASI has an opportunity to complement the Certification program through work with other stakeholders, including Indigenous Peoples and affected communities, to support direct capacity building and amplify positive change in the aluminium value chain.

Desired short-term outcomes (2022-2025)

These strategic foundations aimed to drive ASI towards desired short-term outcomes (2022-2025): rolling out the 2022 Standards launch, continuing to build scale of participation, strengthening engagement with collaborative initiatives and frameworks, and investing in our digital ecosystem to innovatively manage data and stakeholder processes.

Medium term outcomes (2025-2030)

These position ASI for its desired medium-term outcomes (2025-2030): to further evolve its standards and certification program to meet evolving needs, enable access to relevant metrics on progress, and to reach a critical mass for sectoral change at scale (through these and other drivers). The next Standards Revision will be in this timeframe; while the periodic major revision cycle is mapped onto the timeframes to highlight key milestones.

Long term goals (2030-2050)

Together, these outcomes will build the foundations to propel ASI’s members and stakeholders towards our long-term goals (2030-2050) on climate, circularity, nature positive and delivering social value. These goals – and the metrics to support them – will require collective progress and effort across a wide range of programs.

Change is not easy

- We are aiming for global change: though still need to recognise local and context-specific drivers

- We need collective action and shared responsibility: while knowing that individual benefit is often a stronger driver

- We know change pathways are non-linear: so must balance short-term and smaller wins with long-term and big picture goals

- Building trust, consensus and credibility is key: engagement is never finished and must navigate ever-evolving circumstances.

SHARE THIS PAGE: