CRU World Aluminium Summit 2026 Wrap-up: Sustainability continues to shape aluminium markets

The discussions at the Summit reveal that the aluminium industry is increasingly integrating sustainability into how the sector approaches resilience, competitiveness, investment, sourcing and long-term business strategy.

28 May 2026

Set against a backdrop of growing geopolitical uncertainty, shifting trade relationships, CBAM implementation and increasing pressure on global supply chains, one message emerged consistently throughout the Summit: sustainability is no longer being treated as a parallel conversation to aluminium markets and operations. It is increasingly becoming part of how companies manage risk, maintain market access, secure supply, respond to customer expectations and position themselves competitively for the future.

For ASI, co-hosting the Summit together with CRU and the International Aluminium Institute (IAI) highlighted how deeply sustainability considerations are now embedded across mainstream aluminium industry discussions. Alongside dedicated sessions on ASI Standards, responsible sourcing, circularity, climate transition pathways and CBAM implementation, themes such as recycling growth, energy transition, emissions intensity and carbon transparency featured prominently throughout the wider programme.

Discussions throughout the Summit made clear that sustainability is no longer only shaping corporate reporting — it is increasingly influencing trade flows, investment decisions, sourcing strategies and access to markets themselves. The following six themes give a flavour of the discussions and give a sense of how ASI can play a role to support the sector to address some of the key challenges and opportunities it faces.

1. Responsible sourcing becomes a market expectation

One major focus area during the Summit was the rapid evolution of responsible sourcing expectations across aluminium supply chains.

ASI’s Gabriel Carmona Aparicio moderated a session exploring supply chain due diligence and risk mitigation across the aluminium value chain — from bauxite mining through to recycling systems and downstream applications.

Discussions highlighted how due diligence expectations are expanding beyond traditional compliance topics to include climate impacts, human rights, deforestation risks, livelihoods, conflict-sensitive sourcing and increasingly complex sustainability-related data flows.

Particular attention was given to circularity-related due diligence challenges, including the role of informal recycling systems and waste pickers, as well as growing interest in digital product passports, interoperability and digital credential exchange between sustainability systems.

The discussions reinforced that responsible sourcing is increasingly becoming a market expectation linked to credibility, resilience and supply chain access, rather than simply a voluntary sustainability initiative.

Participants also reflected on the growing importance of common frameworks capable of helping organisations compare and assess climate, nature, circularity and human rights considerations across global supply chains.

Key takeaway:

Responsible sourcing is rapidly becoming embedded into mainstream business expectations, customer requirements and market access conditions across the aluminium value chain.

How ASI helps:

Through its multi-stakeholder Standards, Chain of Custody system and ongoing Standards Revision process, ASI is helping build a common framework that supports more consistent, credible and interoperable approaches to responsible sourcing across the sector.

Read the LinkedIn post: Supply chain due diligence and risk mitigation

2. Recycling becomes strategic

Circularity and recycling featured heavily throughout the Summit programme, reflecting growing recognition that secondary aluminium supply is becoming increasingly strategic in an uncertain geopolitical and economic environment.

Moderating the “Closing Loops – Recycling” panel, ASI Circularity Research Manager, Gabriel Carmona Aparicio guided discussions on challenges linked to scrap availability, quality, collection systems, alloy complexity and infrastructure investment.

Drawing on insights discussed in relation to the Circularity Gap Report, panellists explored how tighter competition for high-quality scrap streams, investment in sorting and remelting infrastructure, and efforts by regions and companies to retain valuable aluminium scrap within domestic industrial systems are reshaping aluminium circularity globally.

The discussion highlighted how recycling is increasingly being viewed not only through an environmental lens, but also as an issue linked to industrial resilience, supply security, emissions reduction and long-term competitiveness.

Key takeaway:

Access to high-quality scrap is increasingly becoming a strategic industrial issue — not only for circularity goals, but also for supply security, competitiveness and resilience.

How ASI helps:

ASI’s work on circularity, Chain of Custody and responsible sourcing can help to support greater transparency, collaboration and alignment across increasingly complex material flows and recycling systems — by providing common standards, due diligence frameworks and mechanisms to improve supply chain visibility.

3. Climate ambition meets implementation realities

Climate transition pathways and decarbonisation challenges formed another major area of discussion during the Summit.

ASI’s Climate Change and Decarbonisation Director, Chris Bayliss, participated in a dedicated climate session examining recent sector developments, emissions trajectories, infrastructure constraints and forward-looking transition scenarios.

Drawing on ASI Pathways work and Certified Entity performance data, discussions explored the growing complexity of aligning long-term climate ambition with practical implementation realities across different regions and production systems.

The session highlighted that much of the sector’s recent emissions reductions are currently being driven by changes in production geography and access to lower-carbon electricity, rather than widespread deployment of breakthrough technologies.

Discussions also explored growing concerns around the potential disconnect between corporate climate commitments and the physical availability of lower-carbon aluminium supply — particularly as significant new production capacity emerges in coal-powered regions even while aluminium demand continues to grow as part of the wider energy transition.

The conversations reinforced that many producers remain structurally constrained by slow grid decarbonisation, infrastructure limitations, financing challenges and technology readiness. In this context, standards systems were discussed not as a “silver bullet”, but as a way to increase transparency, accountability and visibility around the trade-offs and realities facing the sector.

A related interview recorded during the Summit with Chris Bayliss explored these tensions more directly, including the challenges of meeting 1.5°C-aligned pathways, the implications of shifting global production capacity, and the role of standards systems in supporting transparency across the aluminium value chain.

Key takeaway:

The aluminium sector faces a growing tension between rapidly rising demand for transition materials and the practical realities of decarbonising production quickly enough to meet climate ambitions.

How ASI helps:

Through its climate criteria, ASI Pathways work and Standards Revision process, ASI is helping drive greater transparency, accountability and dialogue around what credible and achievable transition pathways look like in practice.

Climate transition: An uncomfortable reality check

One of the more candid conversations around CRU World Aluminium Summit 2026 came from ASI’s Climate Change and Decarbonisation Director, Chris Bayliss, in a video interview recorded during the event.

The discussion tackled a difficult tension facing the aluminium sector right now: aluminium is critical for the global energy transition — but major new production capacity is still being built in coal-powered regions.

The interview explores the gap between long-term climate ambition and what is actually happening on the ground today, including:

- the challenge of meeting 1.5°C-aligned pathways

- the reality of slow grid decarbonisation and limited infrastructure

- growing pressure on access to lower-carbon aluminium

- the trade-offs between growth, energy security and emissions reductions

- why transparency and honest conversations around climate pathways matter

It’s a frank discussion about where the climate transition realities remain deeply challenging.

4. CBAM and carbon transparency move into practice

The Summit also highlighted how carbon transparency is increasingly becoming embedded into operational and commercial decision-making.

A dedicated CBAM workshop explored the practical implications of the EU and UK Carbon Border Adjustment Mechanisms for aluminium supply chains, including emissions reporting requirements, customs processes, carbon price exposure and supplier engagement.

Moderated by Chris Bayliss, the discussions reinforced the growing importance of reliable and verified supplier emissions data as CBAM enters its definitive implementation phase.

While CBAM calculations themselves are specific to CBAM legislation, discussions highlighted that broader climate-related management systems, emissions data collection and supplier engagement processes are becoming increasingly important across international aluminium trade flows.

Key takeaway:

Reliable emissions data and stronger supplier engagement are quickly becoming commercial necessities as carbon transparency requirements move from policy into implementation.

How ASI helps:

ASI’s climate-related requirements already support many of the emissions data management, transparency and supplier engagement foundations increasingly needed across international markets and supply chains.

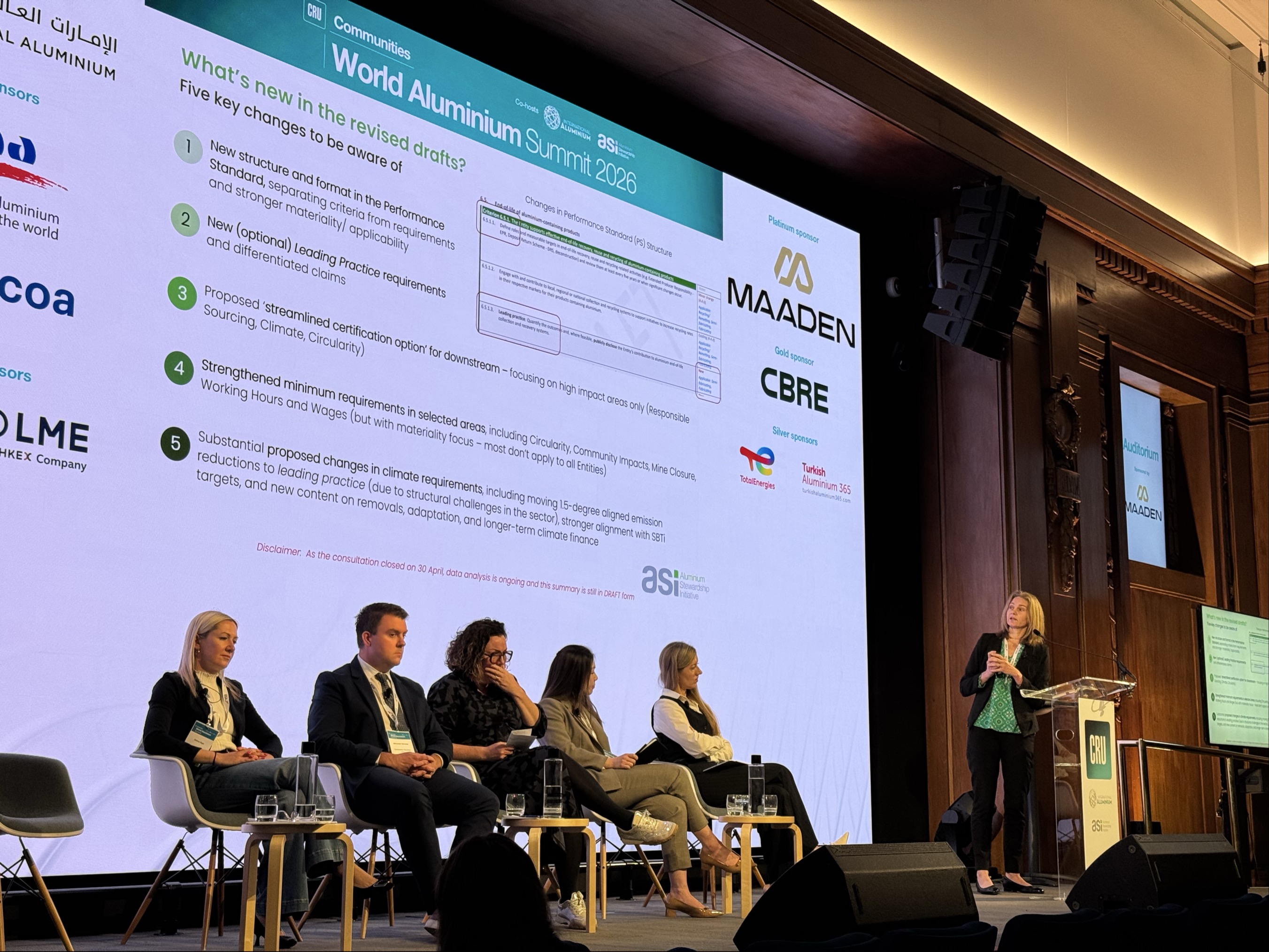

5. The future direction of ASI Standards

The ongoing ASI Standards Revision process also featured prominently throughout the Summit.

Sessions led by ASI Standards Director Chelsea Reinhardt together with ASI Members from across the value chain explored what the 2027 versions of the ASI Performance Standard and Chain of Custody Standard could look like.

Discussions covered major themes emerging from the revision process, including climate ambition, circularity, responsible sourcing, due diligence, materiality and evolving approaches to Chain of Custody and mass balance systems.

A recurring discussion point was the importance of maintaining standards that are both robust and achievable — capable of driving meaningful progress while remaining practical and accessible across different parts of the value chain.

The sessions also reinforced the growing importance of collaboration and alignment across sustainability frameworks, particularly as reporting requirements, customer expectations and regulatory pressures continue to evolve globally.

Key takeaway:

Future sustainability standards will need to balance increasing expectations around climate and responsible sourcing with practical implementation realities across a highly diverse global value chain.

How ASI helps:

ASI uses its convening power to engage with a broad base of sector stakeholders in the current multi-stakeholder Standards Revision process. This lays the foundation for building consensus and ensuring that future requirements remain credible, relevant and implementable across different regions and supply chain contexts.

6. Industry collaboration and leadership

Throughout the Summit, ASI Members shared practical experiences and perspectives from across upstream production, recycling, manufacturing and downstream applications.

The ASI Champions panel brought together representatives from Nemak, SNTO, Constantia Flexibles, Century Aluminum and Novelis to discuss how sustainability expectations are evolving across the sector, the challenges companies continue to face, and how ASI can continue evolving to support meaningful progress.

While panellists highlighted different challenges — including geopolitical disruption, reporting burdens, technology investment needs, data availability and organisational resistance to change — several common themes emerged around the growing importance of harmonisation, interoperability, transparency and collaboration.

As noted during the discussions, many of the sustainability challenges facing the aluminium sector today cannot be addressed by individual organisations acting alone, but instead require collective effort and shared commitment across the value chain.

Key takeaway:

As sustainability expectations continue to grow, collaboration, interoperability and common frameworks are becoming increasingly important across the aluminium value chain.

How ASI helps:

ASI’s multi-stakeholder model helps create a platform for dialogue, alignment and shared action across producers, downstream users, civil society and other stakeholders.

SHARE THIS ARTICLE